A Dallas business owner can go years without hearing the phrase SOX compliance requirements, then one serious growth conversation changes everything. A lender asks tougher diligence questions. A strategic buyer wants control documentation. A new board member asks who can change financial data and how those changes are tracked. Suddenly, what felt like “accounting paperwork” becomes an operational issue involving finance, leadership, and IT.

That shift catches many small and mid-sized businesses off guard. They're not sloppy. They're busy. The company grew faster than the controls did, and now the business needs to prove that its financial reporting can stand up to scrutiny.

Table of Contents

- Your Growing Business and the Sudden Need for SOX

- What Is SOX Compliance Really About

- Decoding the Key SOX Requirements

- Mapping SOX Requirements to Your IT and Operations

- A Practical Readiness Checklist for Your First SOX Audit

- Common SOX Compliance Gaps and How to Fix Them

- Turn SOX Compliance into Your Competitive Advantage

Your Growing Business and the Sudden Need for SOX

A business usually doesn't start with SOX on the priority list. It starts with sales, hiring, delivery, and cash flow. Then growth raises the stakes. The company takes on larger customers, outside investors, acquisition interest, or public-market ambitions. At that point, loose approval chains and undocumented finance processes stop looking efficient and start looking risky.

That's why smart owners should treat SOX as a maturity test, not just a legal burden. The law forces a company to prove that financial reporting is accurate, controlled, and reviewable. It also puts accountability where it belongs. Publicly traded companies spend over $1 million annually on SOX compliance on average, driven by executive certification requirements and independent audits of internal controls according to Pathlock's overview of SOX compliance.

The real pressure point

The cost gets attention, but the bigger issue is executive exposure. If the CEO and CFO have to personally certify reports, “close enough” isn't a strategy. A business either has reliable controls or it doesn't.

Practical rule: If leadership can't explain who approves key transactions, who can alter financial records, and how those actions are logged, the company isn't ready.

For founders navigating capital raises, restructuring, or registration questions, legal preparation matters too. A useful outside perspective is this resource on how to navigate SEC issues as a Miami founder, especially for companies moving from entrepreneurial speed to regulated accountability.

What growing DFW companies should do first

Instead of waiting for an investor, auditor, or buyer to expose gaps, management should do three things now:

- Map financial systems: Identify every system, spreadsheet, storage location, and workflow that touches revenue, payroll, expenses, tax data, or reporting.

- Assign owners: Every control needs a named business owner. Shared accountability usually means no accountability.

- Document approvals: If a process matters financially, approval steps need to be defined and consistently followed.

A Dallas-area SMB doesn't need a giant enterprise bureaucracy. It does need discipline. The companies that handle SOX well are rarely the ones with the biggest budgets. They're the ones that stopped treating internal controls like an afterthought.

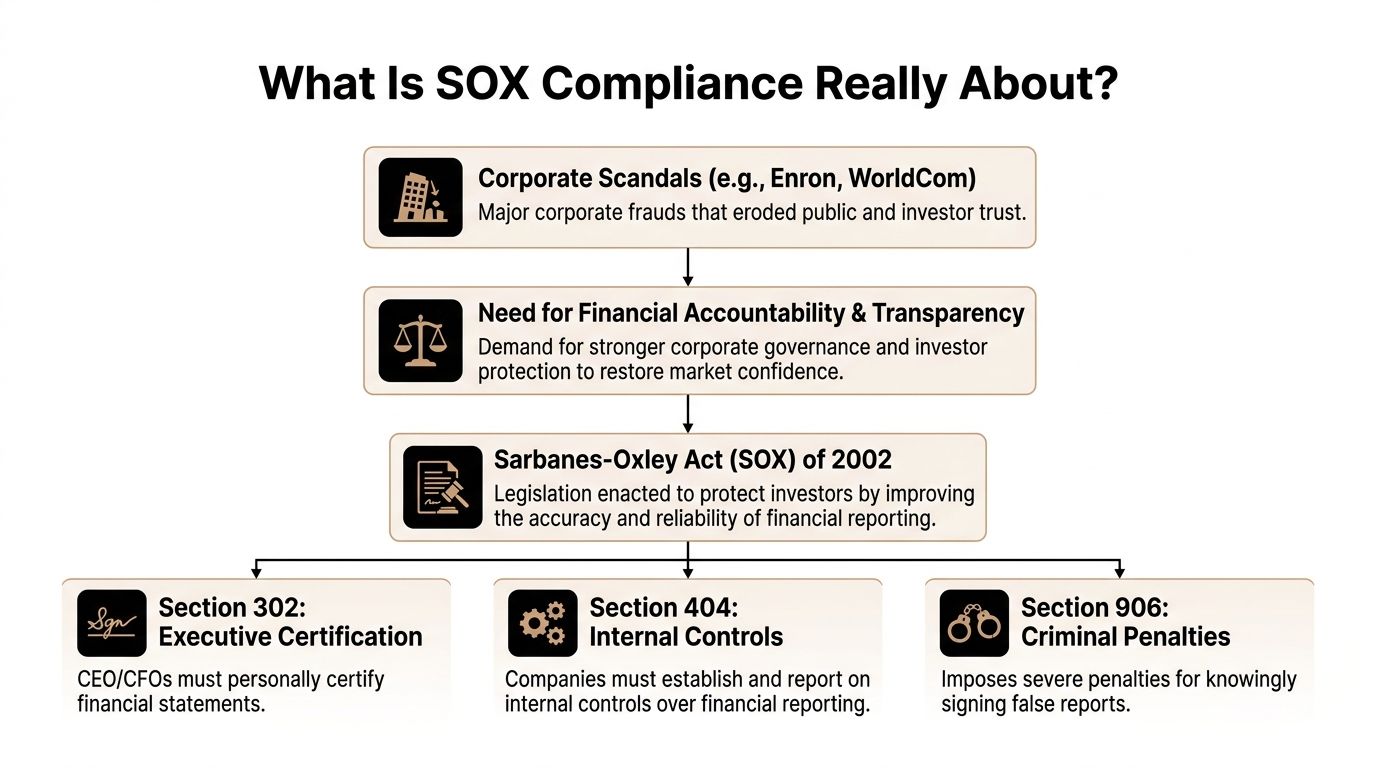

What Is SOX Compliance Really About

SOX exists because trust broke down. Corporate fraud scandals, including Enron and WorldCom, showed what happens when executives can publish financial results without strong oversight, reliable controls, and preserved records. Congress responded with the Sarbanes-Oxley Act of 2002 to restore accountability and protect investors.

Why this law exists

That history matters because it explains the law's posture. SOX assumes financial reporting can't rely on good intentions alone. It requires structure. It requires evidence. It requires independent review.

A useful way to think about SOX is this: it's the building code for financial reporting. A company can't just say the structure is sound. It has to prove the foundation, walls, and inspection process all hold up. In business terms, that means internal controls, documented procedures, protected systems, and outside attestation.

The practical way to think about SOX

Busy owners don't need a law school lecture. They need a plain-English test for whether the company is operating responsibly. These questions get to the heart of it:

- Can the company trust its numbers? Revenue, expenses, assets, liabilities, and disclosures should come from controlled processes, not ad hoc file juggling.

- Can the company prove who did what? Access, approvals, edits, and exceptions should leave a durable trail.

- Can an outside auditor verify the controls? If a process only exists in one employee's head, it doesn't count as a dependable control.

SOX doesn't ask whether the finance team is hardworking. It asks whether the company can demonstrate control over financially significant activity.

That's why IT has a much larger role than many executives expect. Financial integrity now depends on identity management, logging, backup discipline, change control, and data protection. Companies that want a deeper look at how security and compliance intersect can review Technovation's perspective on data security and compliance.

A company that understands this early avoids a common mistake. It doesn't dump SOX onto accounting and hope they can patch the problem with spreadsheets. It builds a control environment that leadership, auditors, and stakeholders can trust.

Decoding the Key SOX Requirements

Most owners don't need every section of the statute memorized. They need to understand the parts that create direct business obligations. Three areas matter most in practice: executive certification, internal controls, and record retention.

Section 302 and executive accountability

Section 302 is the leadership reality check. The CEO and CFO must personally stand behind the company's financial reporting. That changes the tone of the entire organization. If top executives are on the hook, the business needs procedures that reduce guesswork and expose problems early.

That's why informal review habits don't hold up. Verbal signoffs, side spreadsheets, and shared credentials create blind spots. A company needs clear approval paths, role-based access, and evidence that reviews happened.

Section 404 and internal controls over financial reporting

Section 404 is where most of the operational work lives. Management must produce an internal control report assessing whether controls over financial reporting are adequate and effective. Then an independent external auditor must attest to the accuracy of that management statement. That two-layer verification requirement is outlined in Fieldguide's SOX compliance guide.

In plain terms, a company has to do more than claim control. It has to document the controls, test them, and survive outside review.

Typical control areas include:

- Access control: Limit who can view, create, edit, approve, or export financially relevant data.

- Segregation of duties: Separate initiation, approval, and reconciliation tasks so one person can't do everything unchecked.

- Change management: Track and authorize system changes that could affect reports or transaction data.

- Review controls: Require formal review of reconciliations, journal entries, and exceptions.

Section 802 and record retention

Section 802 is often underestimated until it becomes a problem. Public companies must maintain complete financial records for a minimum of seven years, and the law criminalizes destroying those records to impede federal investigations. Auditors also must verify the records are securely protected against alteration for the full retention period, as described in Veza's SOX compliance checklist.

That has direct operational consequences. Retention isn't just “keep some files around.” It means records need to stay accessible, accurate, protected, and tamper-resistant over time.

Bottom line: If a company can't retrieve a financial record with confidence years later, its retention process is weak even if the file technically still exists.

For businesses standardizing cloud records and collaboration workflows, this overview of secure Microsoft 365 compliance strategies is worth reviewing because retention settings, permissions, and auditability often break down in everyday document handling.

A practical reading of Section 802 also raises a modern issue many companies miss. If the business uses automated summaries, generated reconciliations, or system-created logs to support financial reporting, those records need the same seriousness as traditional documents. If the output influences reporting, auditors will care how it was created, stored, and preserved.

Mapping SOX Requirements to Your IT and Operations

SOX becomes manageable once the company stops treating it as abstract law and starts translating it into operational controls. The finance team defines the reporting risk. IT builds and maintains the environment that keeps those risks under control.

Why finance can't handle this alone

A material weakness can start with a technical issue, not an accounting one. Under Section 404, failure to identify and disclose a material weakness, such as a cyber incident causing a 5% or greater variance in financial statements, within 90 days can trigger mandatory Form 8-K reporting within four business days, directly tying security monitoring to executive disclosure duties, according to Flosum's explanation of SOX requirements.

That should end the old argument that cybersecurity is separate from financial reporting. It isn't. If an attack, access failure, or system integrity problem distorts financial data, executives inherit the consequence.

A related lesson appears in other regulated environments too. Companies comparing control mapping across frameworks often find useful overlap in this guide to GDPR and HIPAA. The laws differ, but the operational pattern is familiar: define sensitive data, restrict access, log activity, and prove enforcement.

Mapping SOX rules to practical IT controls

The most effective way to manage SOX compliance requirements is to map each legal obligation to a real control that someone owns.

| SOX Requirement | Objective | Required IT/Operational Control |

|---|---|---|

| Executive certification under Section 302 | Support accurate reporting and leadership signoff | Controlled reporting workflows, documented review steps, approval evidence, restricted edit rights |

| Internal control assessment under Section 404 | Prove controls are designed and operating effectively | Role-based access, segregation of duties, change management, periodic control testing |

| Record retention under Section 802 | Preserve financial records and related evidence | Retention policies, immutable or protected storage, version history, backup validation, access logging |

| Disclosure of material weaknesses tied to cyber events | Surface issues fast enough for required escalation | Security monitoring, incident documentation, escalation procedures linking IT, finance, and leadership |

A business doesn't need a giant compliance platform to start. It needs discipline in a few core areas:

- Access governance: Remove shared accounts, tighten privileged access, and review user rights whenever roles change.

- Logging: Keep logs for key systems that affect billing, payroll, accounting, approvals, and reporting.

- Change control: Require documented approval before modifying financial workflows, integrations, scripts, or reports.

- Incident response linkage: Make sure security events with financial impact reach finance and leadership fast.

Companies trying to align compliance and infrastructure can go deeper with Technovation's approach to compliance solutions for financial services, especially where system access and audit evidence overlap.

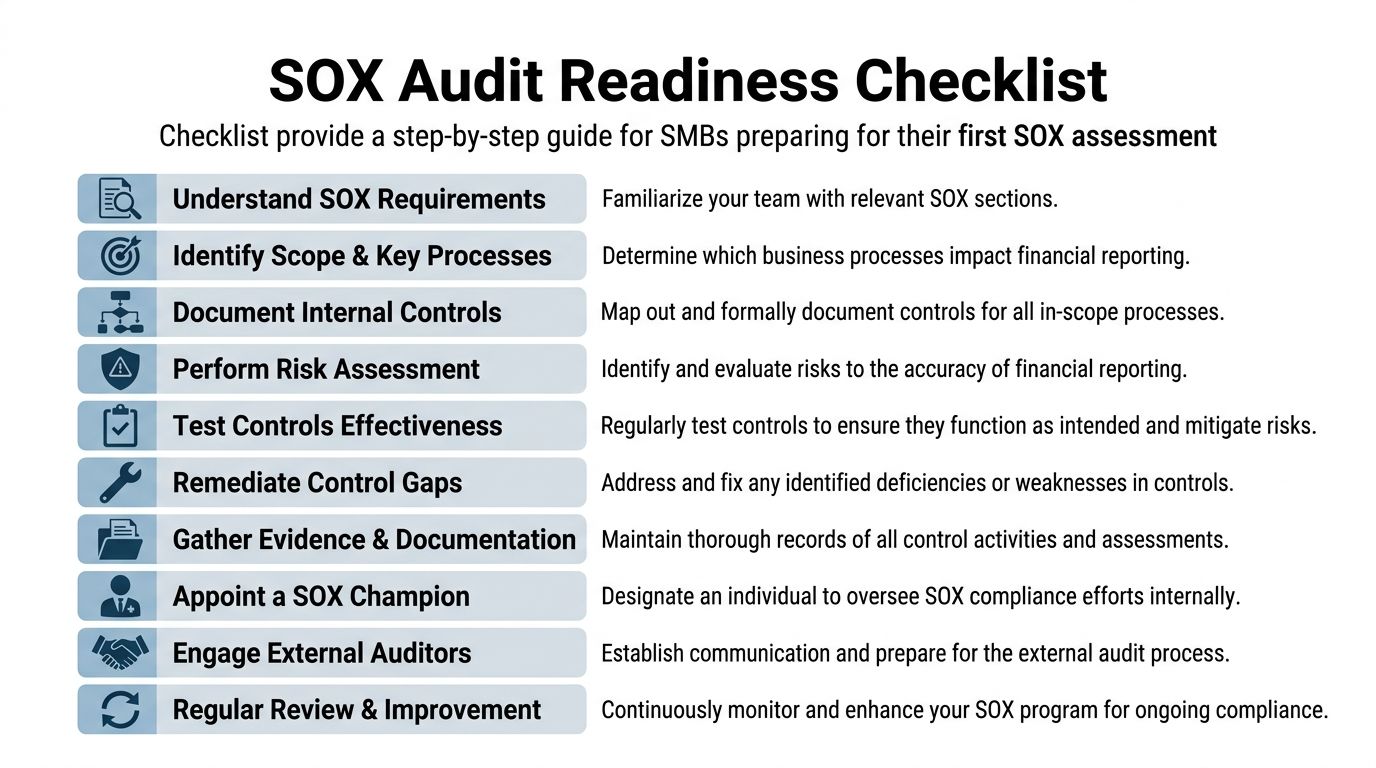

A Practical Readiness Checklist for Your First SOX Audit

It is late in the quarter. Finance is trying to close, your controller is hunting through email for approvals, and your auditor asks for proof that a key report was reviewed and not altered after signoff. If your answer depends on screenshots, memory, or a spreadsheet someone saved to a desktop, you are not ready for a SOX audit.

First-audit readiness is an operations problem, not a paperwork project. The companies that do this well set scope early, assign owners, and collect evidence as part of normal work. They do not wait for the audit request list.

Start with scope and ownership

Begin with the financial reporting chain. Identify the accounts, processes, systems, users, integrations, and outside providers that can change what lands in the general ledger or financial statements. Include manual workarounds, exported spreadsheets, and AI-assisted outputs if anyone uses them to draft entries, summarize transactions, or support reporting decisions.

Then assign ownership. Every key control needs one person to perform it and one person to review it. If nobody clearly owns a control, it will fail when tested.

Use this checklist:

- Define the financial reporting footprint: List the applications, data stores, shared folders, reports, scripts, and manual steps that feed financial reporting.

- Document the high-risk processes: Write down revenue, purchasing, payroll, journal entries, reconciliations, close activities, and approval flows so another employee could follow them without guesswork.

- Mark the control points: Identify where an error, unauthorized change, missing approval, or bad data input could affect reporting.

- Tie systems to evidence: For each control, define what proof you will retain, where it will live, and who can edit or delete it.

- Check digital evidence quality: Make sure logs, approvals, timestamps, version history, and retained records can stand up to auditor review, especially under the PCAOB's AS 1105 audit evidence standard.

Build evidence before anyone asks for it

Section 404 works in two layers. Management must assess internal control over financial reporting, and the external auditor must evaluate management's assessment and test the controls. The SEC explains that framework in its guidance on management's report on internal control over financial reporting. That is why backfilling evidence at audit time usually falls apart.

Collect proof as the work happens.

- Test controls on a schedule: Confirm that approvals, reconciliations, access reviews, and change controls are happening consistently, not just existing in policy documents.

- Retain review evidence in its original form: Save approvals, exception handling records, signoffs, and system-generated logs with timestamps and restricted edit rights.

- Track changes to financially relevant reports and workflows: Preserve who changed what, when they changed it, and who approved it.

- Set rules for AI-generated records: If staff use AI to draft narratives, summarize transactions, or prepare support files, require human review, approval, and retained source documentation.

- Train the people who touch financial systems: They need to know that bypassing a review step or sharing credentials creates an audit issue, not just an IT issue.

- Fix exceptions quickly: A known gap with no remediation plan signals weak control oversight.

Good readiness depends on evidence quality. Auditors will look at whether records are complete, reliable, and protected from casual editing. That matters more now because digital approvals, cloud workflows, and AI-assisted records create new evidence questions that many SMBs still ignore.

A structured IT infrastructure assessment for SOX-sensitive systems helps surface weak logging, poor access control, missing retention settings, and undocumented dependencies before the auditor does.

The first audit goes better when the business treats SOX as a daily operating discipline. Set ownership, tighten evidence handling, and make your systems prove what happened. That is the standard. Technovation helps companies get there without turning the process into chaos.

Common SOX Compliance Gaps and How to Fix Them

Most compliance failures don't come from dramatic misconduct. They come from routine sloppiness that hardens into normal practice. A company may think it has controls because policies exist. Auditors care whether the controls produce reliable evidence.

The hidden problems auditors find fast

Several gaps show up repeatedly in small and mid-sized environments:

- Spreadsheet dependence: Important reviews happen in files passed around by email with no dependable version control.

- Weak user provisioning: Employees keep access they no longer need, especially after promotions, transfers, or departures.

- Untracked changes: Financially relevant reports or workflows get modified without formal approval or retained evidence.

- Messy data classification: Teams don't know which records qualify as financially significant, so retention and protection are inconsistent.

A strong fix starts with inventory and classification. The business should define which systems and records affect reporting, then apply retention, access, and monitoring standards accordingly. A formal data classification policy gives that work structure and keeps teams from relying on guesswork.

Why newer digital evidence rules matter now

Many generic SOX articles often fail to address the rising bar for digital evidence. The emerging AS 1105 standard requires higher rigor for evidence from company information systems, and in 2025, 68% of audit deficiencies were linked to inadequate digital evidence logging, according to Optro's discussion of SOX compliance.

That should change how businesses think about audit preparation. Basic spreadsheets and informal screenshots won't be enough in many environments. If a company relies on system-generated reports, automated workflows, or digital approvals, it needs logging that shows integrity, timing, authorship, and consistency.

There's another modern blind spot. AI-generated financial summaries and automated process logs create retention risk if the business keeps only the final output and not the surrounding metadata or version history. If the record supports financial reporting, the company should preserve the evidence needed to defend how that record was produced.

Operational advice: Treat AI-generated financial artifacts and system-produced summaries like governed business records, not disposable convenience outputs.

The fix is straightforward even if the implementation takes work. Replace informal evidence collection with structured logging. Preserve metadata. Lock down retention settings. Review whether automated outputs can be traced back to source activity. That's the difference between appearing organized and being auditable.

Turn SOX Compliance into Your Competitive Advantage

The strongest companies don't treat SOX as a tax on growth. They use it to tighten operations, improve trust, and make diligence easier. Clean controls reduce confusion. Reliable records support better decisions. Strong access management lowers the odds that one bad permission setting turns into a reporting problem.

That matters in Dallas-Fort Worth because growth opportunities move fast. Buyers, lenders, boards, and major customers don't want promises. They want proof that the business is disciplined enough to scale.

A company that can demonstrate mature controls stands out. It looks better prepared for investment, partnership, acquisition, and expansion. That's the ultimate reward. Better compliance usually means a better-run business.

Technovation LLC helps North Texas organizations turn compliance pressure into practical action. For companies that need a clearer view of their SOX readiness, Technovation LLC offers a complimentary IT health check to identify control gaps, infrastructure risks, and documentation issues before they become audit problems. It's a straightforward way to see where the business stands and what needs to be fixed next.