A lot of small financial firms in Dallas-Fort Worth are operating in a state of constant low-grade tension. Client data is moving through email, file shares, line-of-business apps, and payment systems. Staff members are wearing multiple hats. Meanwhile, every audit request, vendor questionnaire, and policy review feels like a reminder that one weak process can create a very expensive problem.

That pressure is real, but the usual response is wrong. Most firms either overbuy software they won’t use or keep patching together spreadsheets, shared folders, and manual checklists until the whole thing becomes fragile. Neither approach creates confidence. It creates busywork.

The better approach is simpler. Treat compliance as an operating system for the business. Strong compliance solutions for financial services don’t just help with rules. They tighten access, clean up documentation, improve reporting, reduce avoidable mistakes, and make the firm look more trustworthy to clients, examiners, and partners.

Table of Contents

- Navigating the Compliance Maze in Financial Services

- Key Regulations Shaping Financial Compliance

- Translating Regulations into Actionable Controls

- How to Choose Your Compliance Solution Model

- Your Step-by-Step Compliance Implementation Roadmap

- Measuring the ROI of Your Compliance Investment

- The Advantage of a Local Dallas-Fort Worth Compliance Partner

Navigating the Compliance Maze in Financial Services

For many small financial firms, compliance feels like an alphabet soup problem with real consequences. GLBA, PCI DSS, SEC recordkeeping, cybersecurity obligations, audit requests, incident documentation, and internal policies all pile up fast. The result isn’t just confusion. It’s hesitation. Firms delay technology changes, rely on manual workarounds, and hope the current process holds together long enough to get through the next review.

That’s the wrong frame. Compliance isn’t just a defensive exercise. It’s a business discipline that forces firms to clarify ownership, tighten data handling, document decisions, and build repeatable processes. A firm that can prove control over its systems usually runs better day to day than a firm that can’t.

Why smaller firms get stuck

Small and mid-sized firms rarely struggle because they don’t care. They struggle because they don’t have a dedicated internal team for governance, security operations, records management, vendor review, and policy maintenance. One office manager, one operations lead, and one outsourced IT contact can’t carry an enterprise-style compliance burden.

That’s why many firms need a practical standard, not a perfect one. The target should be exam-ready, not overloaded. That means controls are documented, evidence is easy to retrieve, access is managed, incidents are tracked, and leadership can explain how the firm supervises its environment.

Practical rule: If a control can’t be shown to an examiner or auditor with supporting evidence, it probably isn’t mature enough yet.

A more useful way to think about compliance

A strong compliance program does three things at once:

- Protects client trust: Sensitive financial and payment data is handled with clear rules and fewer blind spots.

- Improves internal discipline: Staff members know who approves access, where records live, and how exceptions are handled.

- Supports growth: The firm can respond faster to due diligence requests, client security questions, and audit demands.

That’s why compliance solutions for financial services should be selected and implemented as operating infrastructure. Not as shelfware. Not as a panic purchase after a bad questionnaire. As infrastructure.

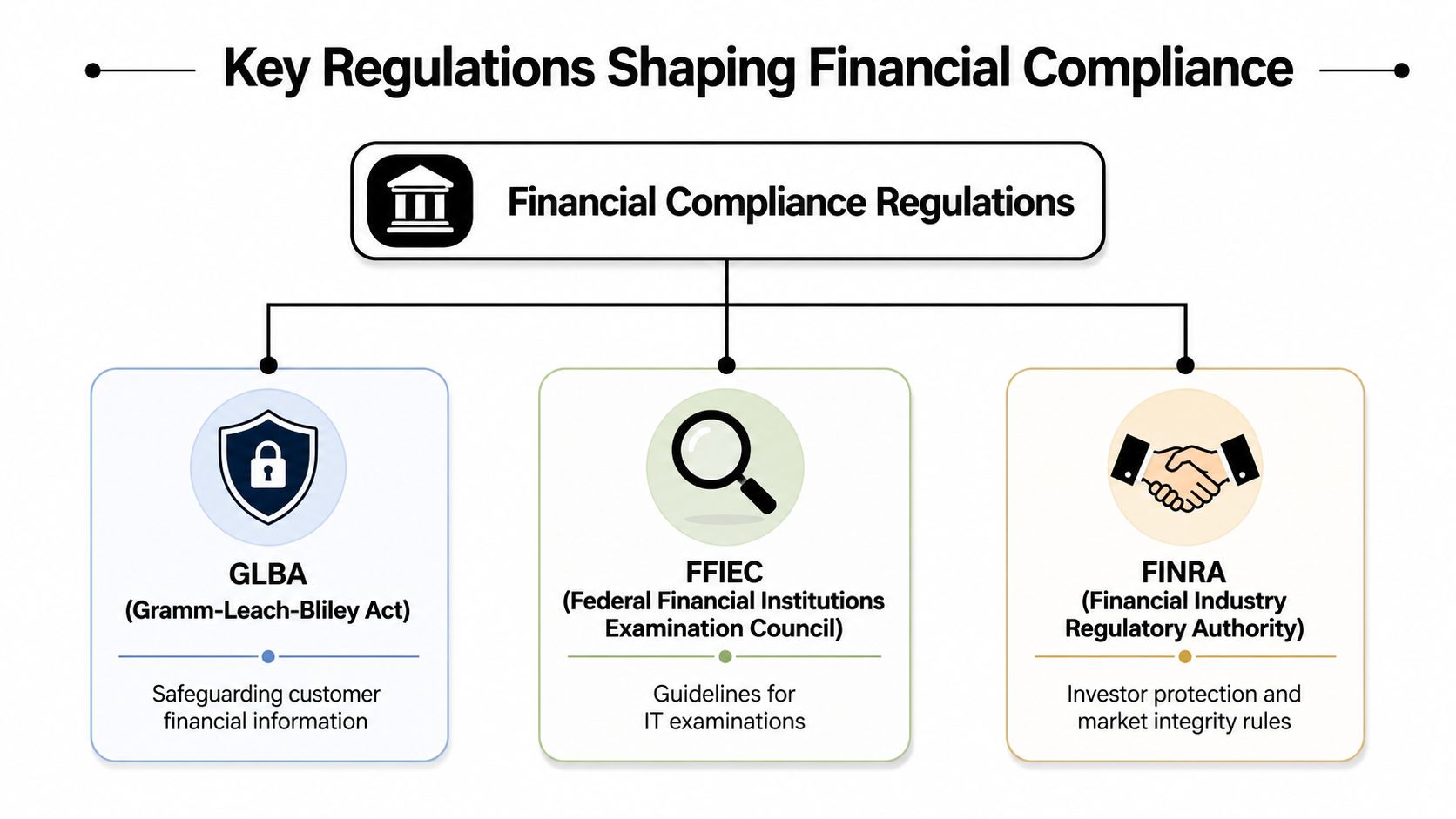

Key Regulations Shaping Financial Compliance

The rules can look disconnected from one another, but most of them push toward the same operational outcome. Regulators want firms to control access, protect sensitive information, retain records properly, monitor activity, and prove that those controls are working.

What regulators actually care about

A lot of owners get lost because they read regulations as legal text instead of operating requirements. The better question is simple. What does this rule require the business to do every day?

A concrete milestone in the evolution of financial compliance tooling was the need to satisfy audit and security obligations under frameworks such as SOX, SEC 17a-4, PCI DSS, and GLBA, with PCI DSS specifically requiring continuous tracking of access to network resources and payment data according to this overview of compliance management tools for financial services. That requirement alone explains why older document repositories aren’t enough anymore. Firms need logging, access control, and review workflows, not just stored files.

Most regulations don’t ask for a fancy platform. They ask for evidence that the firm knows what it’s protecting, who can touch it, and how exceptions are handled.

The rules that shape day-to-day operations

GLBA matters because financial firms are expected to safeguard customer financial information. In plain terms, that affects how the firm stores data, who can access it, how vendors interact with sensitive records, and how incidents are escalated.

SEC 17a-4 matters because record retention and retrievability aren’t optional for firms that fall under those obligations. Messages, records, and supervisory evidence can’t live in random inboxes or unmanaged shared drives if the firm expects to respond cleanly to a request.

PCI DSS matters for any environment that handles payment data. The operational takeaway is direct. Cardholder data requires tighter network discipline, stronger monitoring, and consistent tracking of access to systems and data tied to payments.

SOX pushes firms toward stronger internal control documentation and accountability. Even when a small firm isn’t building a full enterprise control framework, the lesson still applies. Financial processes should have defined ownership, review steps, and evidence.

Cybersecurity rules tied to financial operations matter because security and compliance are now intertwined. Access governance, incident response, retention, encryption, logging, and supervisory review are no longer separate conversations.

For small firms, the smartest move isn’t trying to memorize every citation. It’s mapping each requirement into a few operational categories:

- Access and identity: Who gets access, how it’s approved, and how it’s removed

- Data protection: Where sensitive data sits, how it’s shared, and how it’s secured

- Recordkeeping: What must be retained, for how long, and how it can be retrieved

- Monitoring and review: What activity is logged, who reviews it, and how issues are escalated

- Vendor oversight: Which outside providers touch sensitive systems or data, and what controls govern that relationship

A small financial firm doesn’t need to become a legal think tank. It needs a working control model that lines up with the rules it faces.

Translating Regulations into Actionable Controls

Compliance breaks down when firms treat it like paperwork. Rules only become real when they show up as controls inside systems, workflows, and employee behavior.

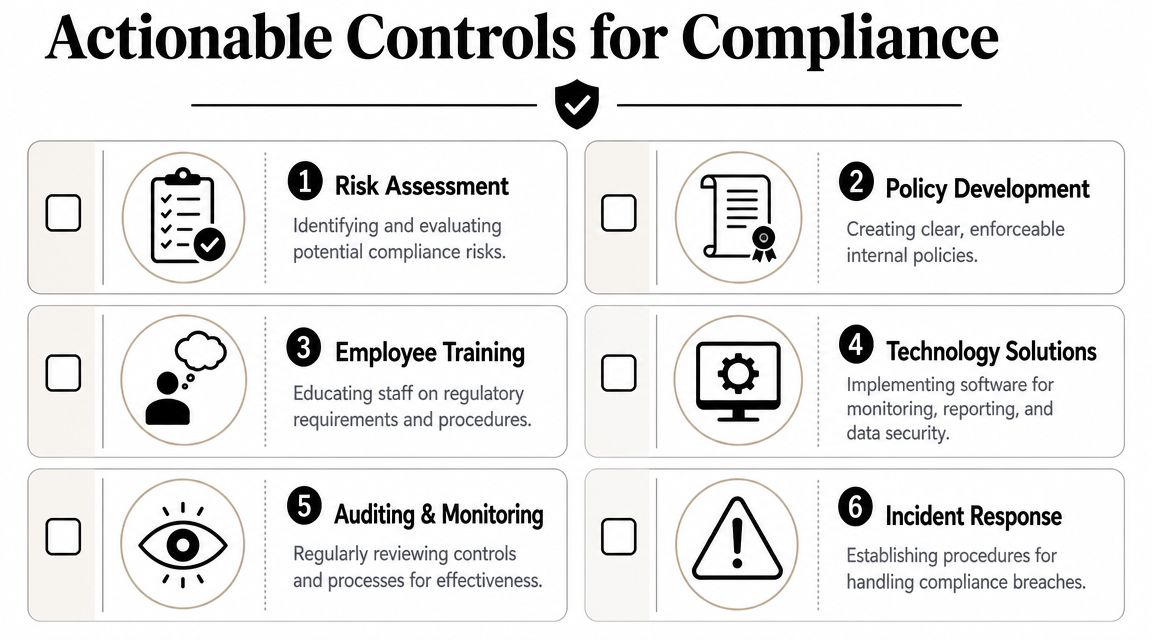

Controls that matter first

The first layer is identity and access management. Every user should have the minimum access needed for the job. Shared accounts should be eliminated where possible. Access approvals should be documented. Departed users should be removed quickly. This is basic, but many firms still get burned here.

The second layer is data protection. Sensitive client and financial information should be protected in transit and at rest. That includes email handling, file storage, device protection, backup discipline, and mobile access. Firms that need a stronger foundation should start with data protection for financial services as a core design principle, not a bolt-on project.

Then comes logging and monitoring. If a firm can’t see access attempts, privilege changes, unusual activity, and system exceptions, it can’t prove control. Logging without review isn’t enough either. Someone has to own review cadence and escalation.

Other controls deserve equal attention, but not equal timing. Start with the ones that reduce the largest exposure fastest.

- Policy development: Written policies should match actual practice. If the policy says quarterly reviews happen, someone should be able to show the last review.

- Endpoint and network hardening: Devices and systems that touch client data need consistent protection, patching, and configuration standards.

- Vendor risk management: Outside providers should be reviewed based on access, criticality, and data exposure.

Why integration matters more than feature lists

The best compliance solutions for financial services don’t sit off to the side. They connect with the systems the firm already uses for banking operations, transaction processing, accounting, and CRM workflows. That matters because effective financial compliance software works by integrating with core systems, generating automated reports from real-time data, and triggering alerts for risky transactions, which reduces manual work and shortens the gap between control failure and remediation according to this guide to financial services compliance software.

That operating model is far more important than a long feature checklist. A small firm doesn’t need five disconnected dashboards that each create a new login and another review queue. It needs a short list of controls that talk to each other and produce usable evidence.

A compliance control is only valuable if staff members can run it consistently and leadership can prove it happened.

A practical control stack usually includes:

- Access controls tied to user roles and approvals

- Protected data flows for documents, email, and stored records

- Activity logging with clear review ownership

- Alerting for suspicious or out-of-policy events

- Retention controls for records and communications

- Incident handling with documented steps and accountability

That’s how regulations become operational. Not through policy binders alone, but through repeatable controls that produce evidence without exhausting the team.

How to Choose Your Compliance Solution Model

Most small firms don’t fail at compliance because they chose the wrong software category. They fail because they chose the wrong delivery model. The daily burden ends up sitting on people who already have full-time jobs.

That’s why the decision should start with operating reality. Who will own the controls? Who will review the logs? Who will keep policies current? Who will support users when access breaks? If the answer to each question is “someone will figure it out,” the model is wrong.

Three realistic paths

The first option is fully in-house. This gives the firm direct control over tooling, policies, reviews, and support. It also demands internal expertise across security, records handling, audit evidence, and day-to-day operations. For a larger firm with a mature internal team, that can work well. For a small office, it often becomes fragile fast.

The second option is a stack of separate cloud tools. This feels modern because each tool handles a specific problem. One for documentation. One for monitoring. One for training. One for retention. One for identity. The problem isn’t the tools themselves. The problem is the seams between them. Someone still has to integrate processes, reconcile evidence, and manage exceptions across systems.

The third option is a managed service model. This works best when the firm wants a practical, maintained environment without hiring a full internal compliance technology team. It aligns especially well with smaller financial organizations that need guidance, implementation support, and ongoing operational discipline.

A common challenge in the market is the mismatch between enterprise-grade tooling and what smaller firms need. The better fit is low-friction, integrated controls that reduce evidence collection burden, and buyers are shifting from isolated feature checklists toward platform cohesion and data lineage according to this banking compliance software analysis.

Compliance Solution Model Comparison

| Model | Initial Cost | Expertise Required | Scalability | Best For |

|---|---|---|---|---|

| In-house build | Higher upfront investment in people, process, and technology | High | Strong if the firm can sustain internal ownership | Firms with dedicated IT, security, and compliance leadership |

| Separate SaaS stack | Moderate to high, depending on how many systems are added | Moderate to high | Can expand, but complexity grows with each added tool | Firms that already have strong internal coordination |

| Managed service model | More predictable operational spending | Lower internal burden | Scales well when controls and support are standardized | Small and mid-sized firms that need exam-ready structure without building everything themselves |

This isn’t a moral choice between independence and outsourcing. It’s a capacity decision.

The right model is the one the firm can operate consistently under pressure, during staff turnover, and during an audit request.

A few decision filters make the choice clearer:

- Choose in-house if the firm already has internal leaders who can own compliance operations, security oversight, and system administration without neglecting the core business.

- Choose a mixed SaaS approach if the firm is disciplined about integration and already has documented workflows for evidence collection, retention, and incident handling.

- Choose a managed model if leadership wants stronger control without adding headcount or stitching together disconnected tools.

Small firms in DFW usually don’t need more software. They need fewer loose ends. That’s why model choice matters more than product demos.

Your Step-by-Step Compliance Implementation Roadmap

Most firms already have pieces of a compliance program. They have policies in a folder, some access controls in place, backups running, maybe a cybersecurity training process, and a rough idea of what records matter. The problem is that these pieces rarely work as a single system.

A structured roadmap fixes that. After the financial crisis, the regulatory wave pushed some banks’ compliance costs up by 60% and accelerated the move away from spreadsheet-driven processes toward integrated platforms that automate controls and support auditability, as noted in this summary of financial compliance challenges. Small firms should take the same lesson without copying enterprise complexity.

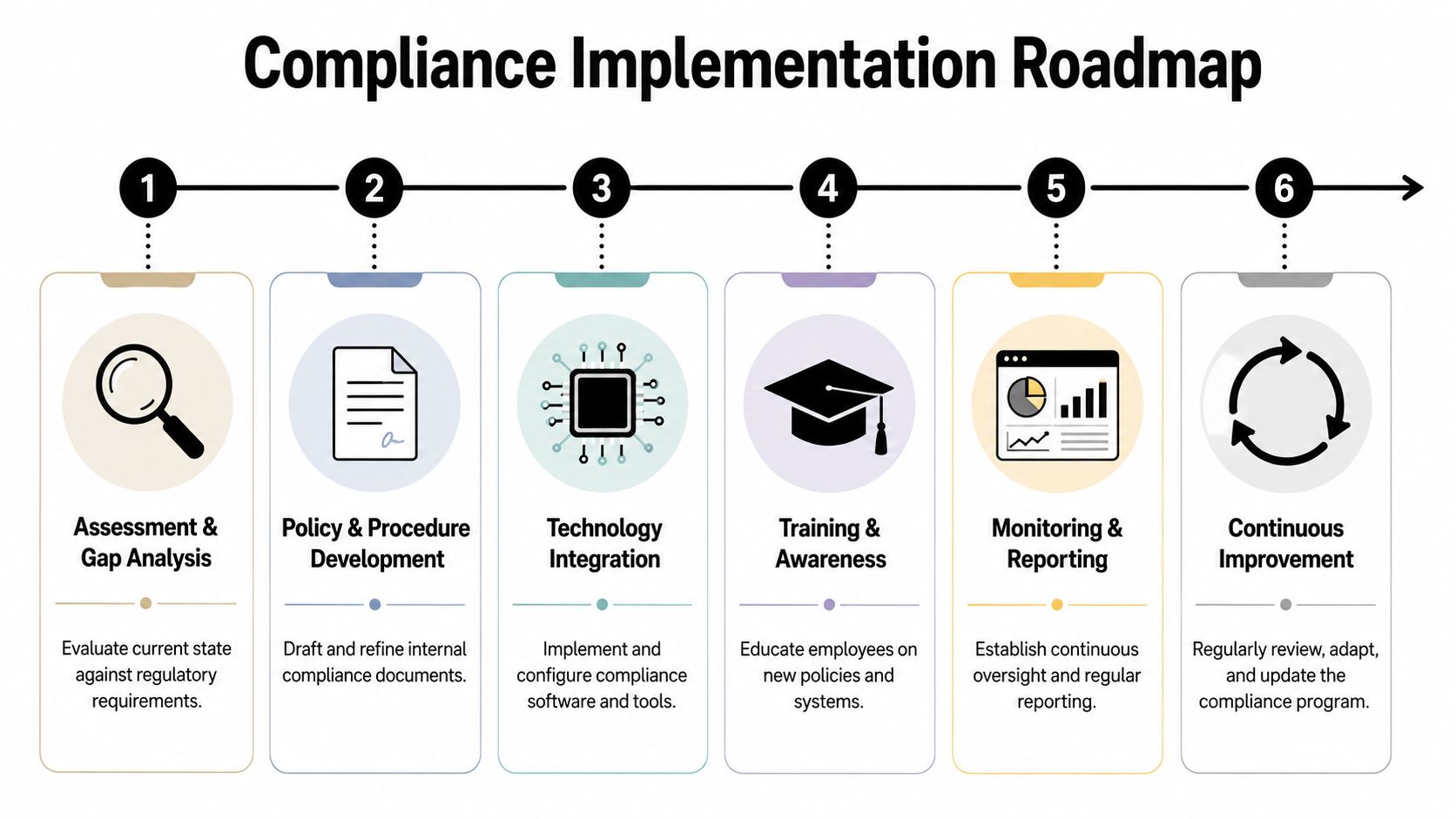

Phase one and two

1. Assessment and gap analysis

Start with the current state. Identify what data the firm handles, which systems store it, which users access it, what records must be retained, and where the biggest process gaps sit. This step should also review vendor relationships, remote access, device security, and logging.

2. Policy and procedure development

Policies should be rewritten around actual operations. Short, usable policies beat long documents nobody follows. Procedures should answer practical questions. Who approves access. Who reviews logs. Who owns retention. Who responds to incidents.

A useful checkpoint at this stage is whether leadership can answer an examiner’s basic questions without guessing.

Phase three and four

3. Phased technical implementation

Don’t try to fix everything at once. Sequence the work. Start with identity controls, data protection, retention, and logging. Then move into workflow automation, exception handling, and deeper monitoring. A phased approach lowers disruption and gives staff time to adapt.

4. Training and accountability

Employees don’t need a legal seminar. They need role-based guidance. Advisors, operations staff, leadership, and support personnel each interact with data and systems differently. Training should reflect that. Just as important, someone should own each recurring control.

5. Ongoing monitoring and reporting

A control that worked during deployment can still fail six months later. Users change roles. Vendors change workflows. New apps appear. Monitoring needs a cadence. Reviews should produce evidence that the firm can retrieve quickly.

6. Continuous improvement

Compliance isn’t a one-time cleanup. It’s maintenance. Policies need updates. Access rights need review. Exceptions need follow-up. Audit findings need closure.

- Start narrow: Focus first on the systems and processes that carry the greatest regulatory and operational weight.

- Document ownership: Every control should have a named owner, even in a small office.

- Collect evidence as work happens: Waiting until an exam notice arrives is what creates panic.

A roadmap matters because it turns compliance from a vague obligation into scheduled work. That alone reduces a lot of unnecessary stress.

Measuring the ROI of Your Compliance Investment

Compliance spending gets dismissed as overhead when leadership only measures it against fines avoided. That’s too narrow. The return shows up in labor efficiency, cleaner audits, stronger client trust, and fewer operational surprises.

Where the return actually shows up

The first return is less manual work. When controls are integrated and evidence is captured automatically, staff members stop wasting hours assembling screenshots, searching email threads, and recreating approval history. That time goes back into client service and revenue-producing work.

The second return is faster issue handling. A compliance process built on continuous monitoring catches problems sooner than a spreadsheet review done after the fact. That matters because response speed often determines whether an issue stays small or expands into an audit headache.

A major trend in the market is the use of AI and machine learning to move compliance from periodic checks to continuous monitoring. These systems can detect unusual patterns in real time and automate reporting, shifting control from reactive to preventive, and for SMBs that means staff can focus on exceptions instead of manual work according to this analysis of AI solutions for regulatory compliance.

What a smarter budget conversation looks like

A practical ROI discussion should look beyond software license cost and ask better questions:

- How much time does the team spend gathering evidence manually?

- How often do access reviews, policy updates, and retention tasks slip because nobody owns them clearly?

- How much friction does the firm create during audits, questionnaires, or client due diligence reviews?

- How much risk comes from delayed detection rather than lack of intent?

Good compliance spending removes recurring friction. That’s where the return gets felt first.

There’s also a reputation dividend. A firm that can answer security and compliance questions clearly tends to look more stable than one that responds with vague language and scattered documents. In financial services, trust isn’t abstract. It affects renewals, referrals, partnerships, and client confidence.

The smartest firms stop asking whether compliance has ROI. They start asking whether their current disorder is costing more than they admit.

The Advantage of a Local Dallas-Fort Worth Compliance Partner

A lot of compliance support looks fine on paper until something goes sideways. Access breaks before a review. A vendor questionnaire arrives with a short deadline. An executive wants a clear answer on record retention, incident escalation, or cybersecurity controls. That’s when distance becomes a problem.

Why local changes the working relationship

A local Dallas-Fort Worth partner works inside the same business environment. That matters more than most firms realize. Local support is easier to reach, easier to hold accountable, and easier to involve in planning conversations that don’t fit neatly into a help desk ticket.

There’s also a practical advantage in having a team that can connect compliance work to everyday IT realities. Financial firms don’t need abstract recommendations. They need help turning policies into operating controls across devices, cloud systems, shared data, user access, and vendor workflows. That’s where IT support for finance becomes part of the compliance conversation instead of a separate function.

What firms should expect from a partner

A useful partner shouldn’t just install tools and disappear. The firm should expect support with priorities that matter:

- Operational clarity: Help identifying the minimum viable control set needed to stay exam-ready

- Evidence discipline: Support building repeatable documentation, review records, and audit trails

- Local responsiveness: Someone who can engage quickly when an issue affects staff, clients, or an upcoming review

- Ongoing alignment: Guidance that adjusts as the business changes, adds staff, or takes on new service lines

National vendors can provide software. Remote providers can provide tickets. A strong local partner provides context. For a small financial firm, that context often makes the difference between a system that looks compliant and one that holds up during scrutiny.

The firms that handle compliance best usually aren’t the ones with the biggest stack. They’re the ones with the clearest ownership, the cleanest workflows, and the fewest gaps between policy and practice.

Technovation LLC helps North Texas financial firms build practical, exam-ready compliance environments without overcomplicating the process. For firms that need stronger controls, cleaner documentation, and a local team that can connect compliance requirements to everyday IT operations, Technovation LLC is a smart next call.