Is a firm's client data being managed like a business asset, or sitting in systems like a liability waiting to be exposed?

That question matters more than most owners want to admit. In financial services, the underlying problem usually isn't ignorance of the rules. Most firms already know they need strong security, careful handling of client records, and documented compliance. The operational gap is elsewhere. They can't consistently prove that the right controls are in place, that third parties are covered, and that someone is watching for issues before an auditor, regulator, or attacker finds them first.

For small and mid-sized firms in Dallas Fort Worth, data protection for financial services has become less about policy binders and more about daily execution. Firms win trust when they can show discipline. They lose it when security depends on memory, manual checks, and outdated assumptions about where sensitive data lives.

Table of Contents

- Why Financial Data Protection Is a Business Imperative

- Understanding Your Regulatory Requirements

- The Evolving Threats to Financial Data in 2026

- A Framework of Essential Protective Controls

- Building a Plan for Risk Assessment and Compliance

- How Managed Services Ensure Your Firm Stays Protected

Why Financial Data Protection Is a Business Imperative

Financial firms don't get the luxury of treating security as back-office overhead. They handle account data, tax records, payment information, personal identifiers, and confidential transactions. That makes data protection a business function tied directly to revenue, reputation, and retention.

The threat environment proves the point. Statista reports that the U.S. financial services industry recorded 744 data compromises in 2023, up from 138 in 2020. That isn't a temporary spike. It's a sign that financial data remains a high-value target and that exposure persists over time.

A firm owner in DFW doesn't need another warning about cyber risk. What they need is a clear conclusion. If a business stores sensitive financial information, then protection of that data belongs in operations, leadership review, and vendor oversight. It can't live only in an annual compliance task.

Practical rule: If client data is essential to serving clients, then protecting that data is essential to running the business.

Strong security also creates opportunity. It helps firms answer due diligence questions from larger clients. It supports cleaner audits. It reduces the chaos that follows a suspected exposure. It also gives leadership a stronger position when evaluating cloud systems, outsourced workflows, and AI-related projects.

Many firms still ask, "Are we compliant enough?" That's the wrong standard. The better question is, "Can this firm prove that sensitive data is controlled, monitored, and recoverable?" That shift changes everything.

Understanding Your Regulatory Requirements

What happens when an examiner, client, or banking partner asks you to prove a control is working today, not just describe it in a policy?

That is where many small and mid-sized financial firms get exposed. They know the rule names. They have written policies. What they often do not have is a clean operating model that assigns ownership, captures evidence, and holds up under audit, vendor review, or a client security questionnaire.

For a DFW firm owner, that gap matters more than the wording of any regulation. Compliance failures usually come from inconsistent execution. A control exists, but nobody reviews it. Access was restricted once, but no one revalidated it after staffing changes. Logs are enabled, but nobody can produce them quickly. Those are operational failures, and they create legal and business risk.

What GLBA means in daily operations

GLBA pushes firms toward disciplined handling of customer information. In practice, that means you need to know where sensitive data lives, who can access it, how changes are approved, and what proof shows those controls are active. If your team cannot answer those questions without chasing screenshots and old emails, your compliance process is weak.

Use these questions as a management test:

- Data location: Which systems store client financial records, supporting files, exported reports, and backups?

- Access control: Which employees, contractors, and outside providers can see, copy, or send that data?

- Change management: Who approves new apps, file-sharing methods, integrations, and remote access?

- Evidence: Which logs, review records, tickets, and policy acknowledgments prove the controls are running?

A privacy-focused operational checklist can help tighten that process. This CCPA compliance checklist from Technovation is useful because it forces firms to map data, ownership, and response steps in a way leadership can review and defend.

Compliance is proven with records, ownership, and repeatable execution.

What PCI DSS changes for firms that accept cards

PCI DSS is more prescriptive, which helps. If your firm accepts payment cards, cardholder data must be protected in storage and during transmission. Encryption is the baseline. So is control over who can access payment data, how long it is retained, and how the environment is monitored.

That requirement should shape daily decisions, not just annual paperwork.

| Operational area | What it means in practice |

|---|---|

| Key management | Encryption fails if keys are shared loosely, stored carelessly, or never rotated. |

| Data retention | Extra card data creates extra liability. Keep only what the business and the standard require. |

| Authentication | Weak passwords, shared accounts, and missing MFA give attackers an easy path around technical controls. |

| Testing and monitoring | Firms need regular verification that protections are working and alerts are reviewed. |

Here is the point firm owners should act on. Regulations tell you what outcome is expected. Your business still needs a way to assign control owners, document reviews, collect evidence, and fix exceptions before they become findings. For many SMB financial firms, that is the exact gap a managed service partnership closes. It turns compliance from a yearly scramble into an operating process you can verify.

The Evolving Threats to Financial Data in 2026

The old threat model was simple. Keep outsiders off the network and the problem is mostly solved. That model is dead.

Financial firms now deal with a layered attack environment. Attackers don't just target servers. They target users, cloud workflows, shared drives, remote access, vendor accounts, AI tools, and the trust relationships between them. A clean firewall rule doesn't help much if an employee uploads sensitive information into the wrong application, or if a convincing fake message gets a controller to approve the wrong request.

Why old assumptions fail

The threat environment has changed because the technology environment has changed. Financial firms adopted cloud systems, remote work, mobile access, outsourced support, and AI-assisted workflows. Sensitive data now moves through more places, and every handoff creates another exposure point.

The complexity is visible in current security operations. The 2026 Thales Data Threat Report for Financial Services found that 79% of organizations had five or more data protection tools, 48% had five or more key management systems, and only 32% said they had complete knowledge of where their data is stored. More tools haven't automatically created more control.

That same report shows where the pressure is moving. 64% of organizations experienced prompt injection attacks on AI applications, 62% reported sensitive data disclosure, and 60% reported deepfake attacks. The message is clear. Attackers are exploiting behavior, automation, and fragmented environments, not just old infrastructure weaknesses.

How modern attacks hit real firms

A financial firm doesn't need a dramatic movie-style breach to have a serious incident. A few realistic examples show the problem:

- Executive impersonation: A staff member receives an urgent voice message or video call that appears to come from leadership and authorizes a transfer, account change, or records release.

- Cloud leakage: A shared repository or file sync location contains exported reports with client information and broader permissions than anyone realized.

- AI misuse: An employee pastes customer details into an AI tool to summarize notes or draft a response, then sensitive information leaves the controlled environment.

- Credential abuse: An attacker gets access through reused passwords, missing MFA, or stale third-party accounts that no one disabled.

The firms most at risk often aren't the firms with no tools. They're the firms with disconnected tools, weak ownership, and no one looking across the whole environment.

The takeaway for data protection for financial services is simple. Security has to follow the data. It can't stop at the perimeter, the office, or the server room. If the business uses the data, the business has to control how that data is accessed, shared, monitored, and recovered.

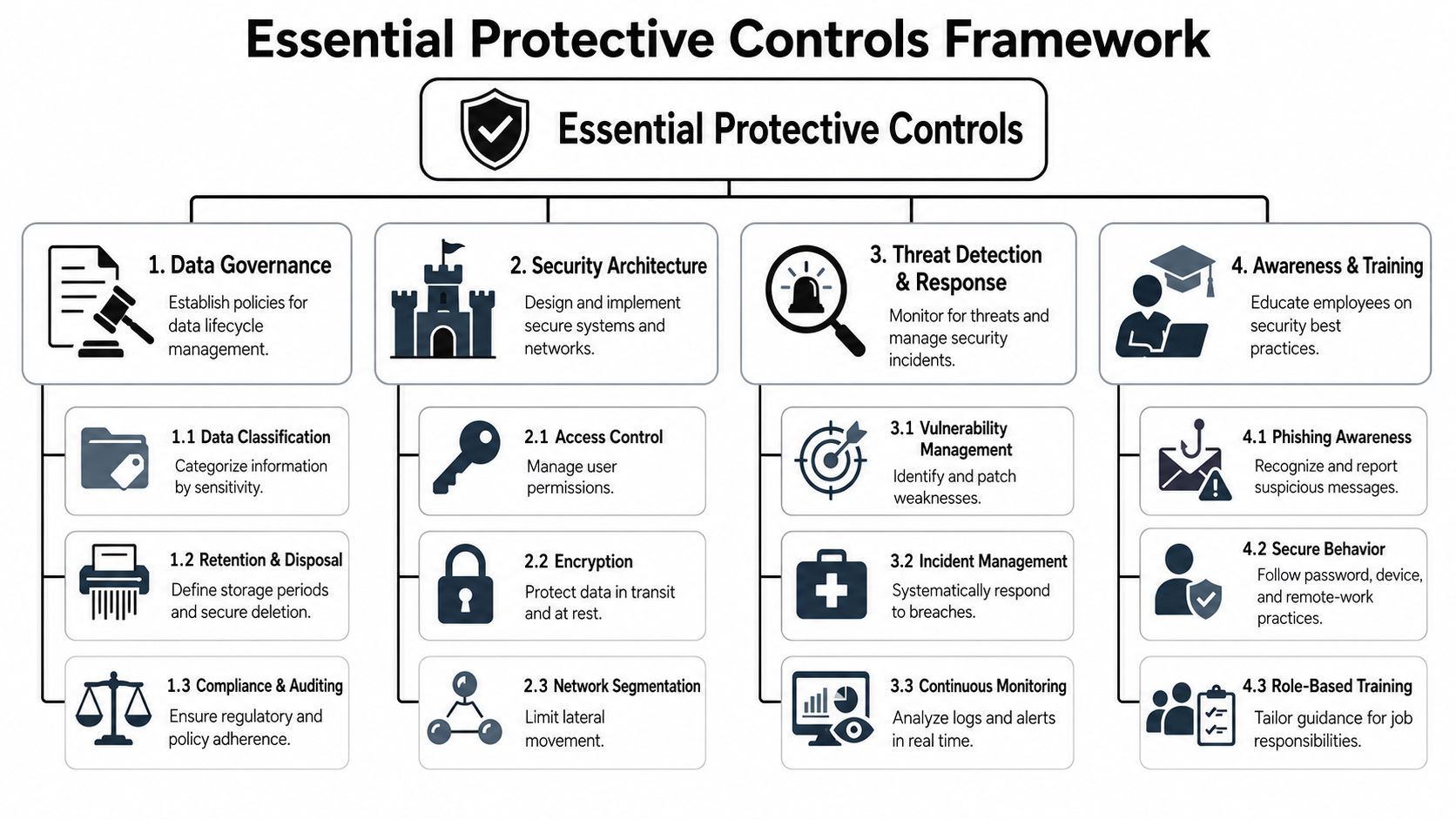

A Framework of Essential Protective Controls

What does your firm control today, and what could you prove to an auditor tomorrow? Those are not the same question. Financial firms usually know the rules. The operational gap shows up when they cannot show who has access, where regulated data lives, whether backups work, or which controls are reviewed on a schedule.

A control framework should do three jobs well. Limit access. Protect the data wherever it lives. Produce evidence that the controls are active, tested, and owned.

Start with access control

Access is the first control to tighten because it affects every system that holds client, payment, tax, or investment data. If too many people have broad access, one stolen password or one bad approval turns into a much bigger problem.

Use a simple model and enforce it:

- Role-based permissions: Give employees access based on job function, not convenience.

- MFA on every sensitive system: Email, remote access, cloud apps, admin accounts, and finance platforms should all require more than a password.

- Joiner, mover, leaver controls: Access changes should happen immediately when someone is hired, changes roles, or leaves.

- Separate privileged accounts: Admin work should happen from dedicated accounts, not the same accounts used for daily email and browsing.

This is also where firms start to separate “we have a policy” from “we can prove control.” You should be able to pull an access review, show approvals, and explain exceptions without a scramble.

Protect the data directly

Perimeter security matters, but it does not answer the main question regulators and clients care about. What protects the data itself?

Use a short list of controls and apply them consistently:

| Control | Why it matters |

|---|---|

| Encryption | It reduces exposure if data is intercepted, copied, or accessed without approval. |

| Secure backups | They support recovery after ransomware, deletion, corruption, or human error. |

| Data classification | It tells your team which records need tighter handling and higher oversight. |

| Retention limits | It removes old data that creates risk without adding business value. |

Treat encryption as a baseline control for regulated financial data, not a special project. Apply it to data in transit, at rest, on endpoints, in cloud storage, and in backup systems. Then document where encryption is enabled, who manages the keys, and how you verify the setting stays in place.

Classification and retention matter just as much. Firms lose control when sensitive files spread across desktops, inboxes, shared folders, and ad hoc exports. Every extra copy creates more review work, more exposure, and more evidence you may not be able to produce later.

Decision test: If your team cannot explain why a sensitive record is stored in a location, remove it from that location.

Make monitoring and response part of operations

Controls fail without warning when nobody owns the daily work. Patches slip. Alerts pile up. Backup errors go unnoticed. Logging exists, but nobody checks whether it captures the events that matter.

Focus on three operating disciplines:

First, system hardening and patching. Endpoints, servers, network devices, and cloud workloads need secure configurations and a defined patch cycle.

Second, logging and alert review. Record access to sensitive data, permission changes, failed logins, suspicious file sharing, and unusual account behavior. Keep logs long enough to support investigations and compliance reviews.

Third, staff guidance and response playbooks. Give employees direct instructions for payment change requests, document handling, account lockouts, and suspected fraud. If the response depends on memory, it will break under pressure.

This operating layer is where many SMB financial firms get stuck. They know what controls should exist, but they do not have the time or internal depth to run them consistently and preserve evidence. A managed service partnership closes that gap by handling the day-to-day control checks, documenting the work, and keeping security tied to actual business risk. Technovation LLC, for example, provides managed IT, compliance support, cloud backup, and continuous monitoring for regulated organizations in North Texas.

A useful framework is not complicated. It is assigned, enforced, reviewed, and documented. That is how a firm protects data and proves it.

Building a Plan for Risk Assessment and Compliance

Security controls without a management plan turn into a pile of disconnected tasks. A firm might have MFA, backups, and endpoint protection in place and still fail an assessment because it can't show risk ownership, vendor oversight, or repeatable review.

The better approach is to treat compliance as an operating cycle. The firm identifies where sensitive data lives, decides what level of protection each environment needs, verifies the controls, and updates the process when systems or vendors change.

Start with evidence not assumptions

A useful risk assessment is specific. It doesn't ask whether security exists in general. It asks where client data is stored, how it moves, who can access it, and what could expose it.

A practical review should cover:

- Systems and repositories: Core business apps, file shares, cloud storage, endpoints, archived data, and backups.

- User access: Employees, contractors, outsourced staff, and dormant accounts.

- Business processes: Client onboarding, file exchange, payment workflows, remote work, and report generation.

- Failure scenarios: Account compromise, accidental disclosure, lost devices, ransomware, and vendor outages.

This process usually exposes a pattern. Firms often know their main systems well, but the side paths create problems. Exports, temporary files, shared folders, personal devices, and third-party portals are where clean policy language breaks down.

Treat vendor risk like internal risk

Third-party exposure is one of the most overlooked issues in financial services. Firms hand data to cloud applications, payment processors, outsourced IT providers, document platforms, and specialized service vendors. That doesn't transfer accountability.

That has real consequences for owners. Vendor management can't stop at signing a contract. It needs operating discipline.

| Vendor oversight question | Why it matters |

|---|---|

| What data does the vendor receive? | Scope determines risk. |

| How is it protected? | Security claims need documentation and review. |

| Who can access it? | Shared access creates hidden exposure. |

| What happens after an incident? | Contracts should define notification, responsibility, and response expectations. |

A firm doesn't need perfect visibility into every supplier. It does need enough visibility to prove due diligence and make defensible decisions.

Use a repeatable operating cycle

Strong compliance programs usually follow the same rhythm:

- Identify sensitive data, systems, users, and dependencies.

- Protect them with access control, encryption, backups, and policy enforcement.

- Detect unusual activity, misconfigurations, and exposure events.

- Respond with documented escalation and decision-making.

- Recover through tested restoration, communications, and post-incident review.

A firm that only checks controls before an exam doesn't have a compliance program. It has a scheduling habit.

For business owners, the win is consistency. When reviews, approvals, testing, and vendor checks happen on a defined cycle, the firm moves from scrambling to governing.

How Managed Services Ensure Your Firm Stays Protected

Most small and mid-sized financial firms already know what good security looks like in theory. The problem is keeping it working every week without dropping core client work.

That is why managed support makes sense. The need isn't just technical labor. It's operational continuity. Someone has to maintain monitoring, review alerts, document controls, track changes, support audits, manage backups, and make sure the environment still matches the firm's risk profile.

Why internal effort usually stalls

Many owners assume a capable office manager, internal administrator, or part-time consultant can keep security and compliance on track. Usually, that works until the environment changes. A new cloud app gets approved. A vendor needs access. A team starts using AI tools informally. Remote staff expand. An insurance renewal asks tougher questions. Then the gap appears.

The issue isn't effort. It's bandwidth and specialization.

A firm that wants defensible data protection for financial services needs ongoing execution in areas like these:

- Continuous monitoring: Security events must be reviewed as they happen, not months later.

- Control validation: Backups, access rights, endpoint protections, and alerts need regular testing.

- Documentation: Policies, evidence, incident records, and vendor reviews need to stay current.

- Strategic alignment: Security settings should reflect how the business handles data, not how it worked two years ago.

Point-in-time checkups fall short for this exact reason. Regulatory guidance increasingly aligns with frameworks like the NIST CSF and emphasizes continuous monitoring, which means SMBs need real-time discovery and response rather than periodic reviews alone.

What a managed partnership should actually deliver

A managed service partnership should do more than install tools. It should create an operating model the firm can defend.

That means owners should expect support in four areas.

First, visibility. The provider should help the firm understand where sensitive data lives, which systems are critical, and where exposure can occur.

Second, control operation. Access management, backup oversight, patching, endpoint protections, and monitoring need active management, not passive deployment.

Third, compliance readiness. The provider should help translate security work into evidence, reviews, and documented procedures that hold up under scrutiny. Firms evaluating managed IT support for finance from Technovation are usually looking for that bridge between technical controls and provable compliance.

Fourth, local responsiveness. For DFW firms, local support still matters. Security decisions affect operations, client service, and leadership accountability. A nearby partner can move faster when a situation needs escalation, coordination, or direct planning with firm leadership.

A managed relationship also improves decision quality. Instead of reacting after an alert, outage, or audit request, the firm gets a structured cadence for review, remediation, and planning. That is how risk becomes manageable.

The right question for a financial services owner isn't whether the firm has some security tools in place. The right question is whether anyone is accountable for keeping the whole system controlled, documented, and audit-ready every day.

Financial firms in North Texas don't need more vague advice about cyber risk. They need a clear operating model that protects client data, supports compliance, and stands up to real scrutiny. Technovation LLC helps regulated organizations close the gap between knowing the rules and proving they're being followed through managed IT, cybersecurity, compliance support, and continuous monitoring. A practical next step is a security audit or IT health check to identify where sensitive data is exposed, where controls are weak, and what needs to be fixed before it becomes a business problem.